Moving a loved one into assisted living rarely happens on a perfectly timed financial schedule. More often, it feels like trying to leap across a river with your foot still stuck on the dock. That’s where bridge loans come in.

A bridge loan for assisted living is a short-term loan designed to “bridge the gap” between needing care now and having funds available later, usually from selling a home or accessing other assets.

Let’s break down how they work, when they make sense, and what to watch out for.

What Is a Bridge Loan for Assisted Living?

A bridge loan is a temporary financing option that gives families immediate access to cash to cover:

- Assisted living entrance fees

- Monthly care costs

- Moving expenses

These loans are most commonly used when a senior has significant equity tied up in their home but hasn’t sold it yet.

Think of it as financial scaffolding. It holds things up while the permanent structure (like a home sale) gets completed.

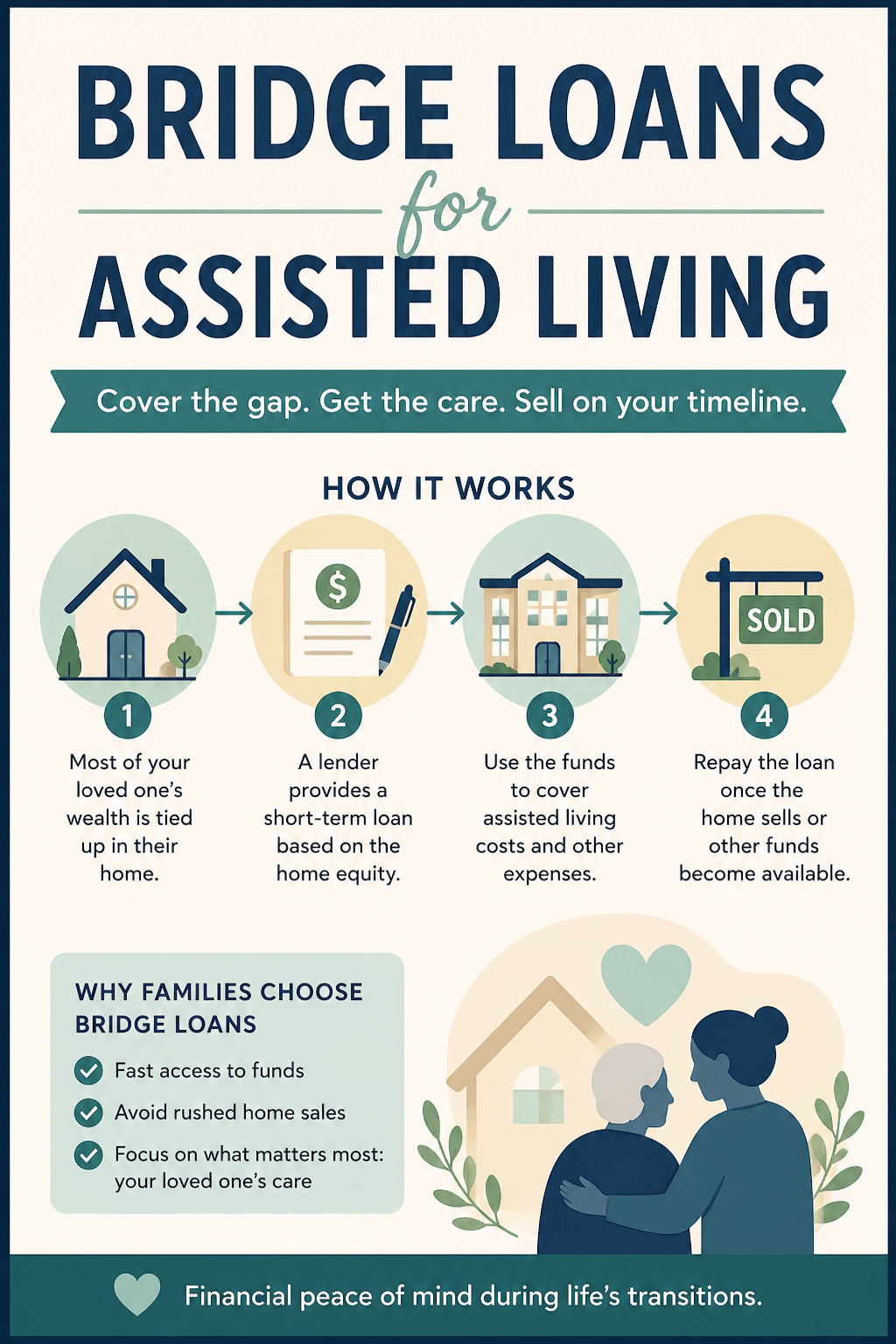

How Bridge Loans Work

Here’s the typical flow:

- A loved one needs to move into assisted living quickly

- Most of their wealth is tied up in a home

- A lender provides a short-term loan based on that equity

- The loan is repaid once the home sells or funds become available

Loan terms are usually short, often 6 to 12 months, sometimes up to 24.

Some lenders offer interest-only payments, while others allow you to defer payments entirely until the loan is repaid.

When a Bridge Loan Makes Sense

Bridge loans can be helpful in situations like:

- Urgent care needs after a hospital stay

- Delays in selling a home

- Family disagreements about timing or logistics

- Avoiding rushed home sales at below-market prices

Instead of accepting the first low offer just to free up cash, a bridge loan buys you time to sell strategically.

Pros of Bridge Loans

Bridge loans can feel like a financial pressure valve releasing steam at just the right moment.

Key advantages include:

- Fast access to funds

- Allows for a smoother transition into care

- Prevents rushed or undervalued home sales

- Flexible repayment options in some cases

Cons to Consider

This convenience comes at a cost, and it’s important to look at the full picture.

Potential downsides:

- Higher interest rates than traditional loans

- Fees and closing costs

- Risk if the home doesn’t sell quickly

- Short repayment timelines

If the home lingers on the market longer than expected, the loan can become a heavier burden.

Alternatives to Bridge Loans

Before committing, it’s worth comparing other options:

Home Equity Line of Credit (HELOC)

If there’s time to set it up, a HELOC can offer lower interest rates.

Reverse Mortgage

A reverse mortgage allows seniors to tap into home equity without monthly payments, but it comes with long-term implications.

Personal Savings or Family Contributions

Sometimes families pool resources to cover short-term costs.

Selling the Home First

If timing allows, this avoids borrowing altogether, though it’s not always realistic.

What to Look for in a Lender

Not all bridge loans are created equal. When comparing options, pay attention to:

- Interest rates and total cost

- Repayment structure

- Loan term flexibility

- Fees and penalties

- Experience with senior care financing

Some lenders specialize in senior transitions and may offer more tailored terms.

Is a Bridge Loan Right for Your Situation?

A bridge loan isn’t a magic solution, but in the right scenario, it can ease one of the most stressful transitions a family faces.

If you’re balancing urgency with financial logistics, it can provide breathing room when you need it most.

The key is to go in with clear expectations. Know your repayment plan, timeline, and backup options.

Because when it comes to assisted living decisions, peace of mind is just as valuable as the numbers on paper.

FAQs About Bridge Loans for Assisted Living

How fast can you get a bridge loan?

Some lenders can fund loans in just a few days, especially if the home equity documentation is straightforward.

Do you need good credit?

Credit matters, but lenders often focus more on the home’s equity and expected sale value.

What happens if the home doesn’t sell in time?

You may need to refinance, extend the loan, or explore other funding sources.

Are bridge loans only for homeowners?

Typically yes, since they rely on home equity as collateral.

Final Thoughts

Bridge loans sit in that in-between space, not permanent, not ideal, but sometimes exactly what’s needed. Like a temporary bridge over fast-moving water, they’re built for crossing, not staying.

Used wisely, they can turn a stressful, rushed decision into a more thoughtful transition for everyone involved.