Buy now, pay later apps are everywhere these days. From checkout pages to smartphone apps, it seems like every retailer wants shoppers to split purchases into smaller payments. One company gaining attention in this space is Zilch.

But what exactly is Zilch, and how does it work?

If you’ve seen the name pop up online or wondered whether it’s different from services like Klarna or Afterpay, here’s a closer look at the platform, its features, and some things consumers should know before using it.

What Is Zilch?

Zilch is a buy now, pay later (BNPL) platform that allows shoppers to split purchases into installments or delay payments. The company launched in the UK and has expanded its financial technology offerings over time.

Unlike some BNPL services that are tied directly to specific retailers, Zilch operates more like a virtual payment layer. Users connect a debit card to the app and can then use Zilch to pay at participating retailers or anywhere Mastercard is accepted.

The platform markets itself as a flexible alternative to traditional credit cards, especially for shoppers who want predictable payments.

How Does Zilch Work?

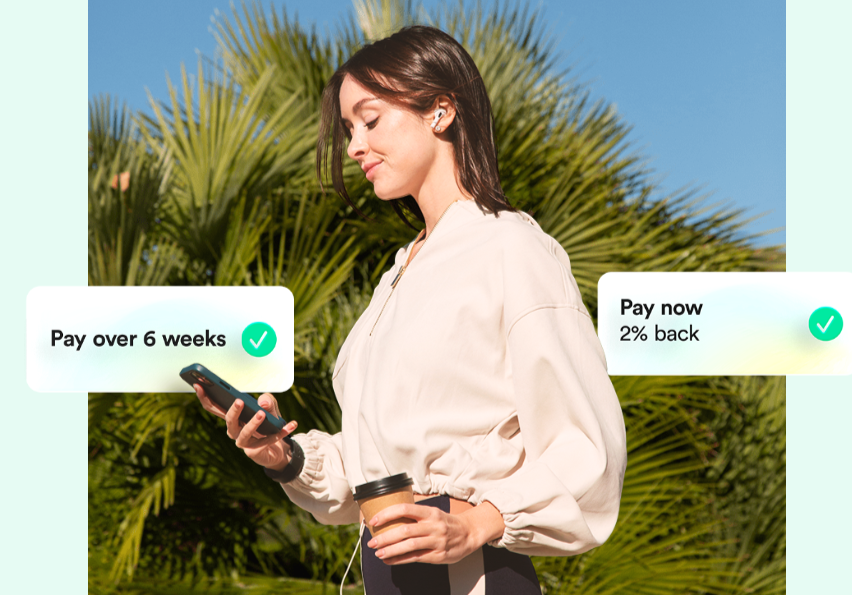

After downloading the app and creating an account, users are typically offered several payment options:

- Pay in full immediately

- Split a purchase into four installments

- Delay payment for a later date

- Use rewards or cashback offers on eligible purchases

For installment plans, the total cost is usually divided into four payments spread over several weeks. Some purchases may include fees or interest depending on the payment option selected.

Zilch also issues a virtual card that can be added to digital wallets like Apple Pay or Google Pay.

The process feels a bit like turning your debit card into a mini financing tool. Instead of paying all at once, shoppers can stretch costs across multiple payments.

Where Can You Use Zilch?

One feature that makes Zilch stand out is its broader payment flexibility.

Some BNPL providers only work with approved merchants at checkout. Zilch’s virtual card setup allows users to shop at many more stores, including both online and in-person retailers that accept Mastercard.

That means users can potentially use Zilch for:

- Clothing purchases

- Electronics

- Travel expenses

- Household items

- Everyday shopping

Still, availability varies by region and merchant restrictions may apply.

Does Zilch Charge Interest?

This depends on the payment option selected.

Some “Pay in 4” purchases may be interest-free if payments are made on time. However, missed payments or longer financing options can include fees.

Like most BNPL services, the convenience can become expensive if balances pile up.

Consumers sometimes treat BNPL apps like invisible money because the payments seem smaller. But four small payments across five different apps can quickly snowball into a very real budget problem.

Is Zilch a Credit Card?

Not exactly.

Zilch is considered a fintech payment platform rather than a traditional credit card issuer. However, some features can resemble a credit product because purchases may involve borrowing money temporarily.

Depending on the country and regulations, Zilch may perform eligibility checks or report certain payment behavior to credit agencies.

That’s why users should still treat BNPL services carefully. Even if something doesn’t look like a credit card, it can still affect financial habits and possibly credit history.

Why BNPL Platforms Became So Popular

Apps like Zilch exploded in popularity for a few reasons:

Smaller Payments Feel Easier

Breaking a $200 purchase into four $50 payments feels psychologically lighter, even if the total cost is the same.

Younger Consumers Avoid Credit Cards

Many younger shoppers prefer BNPL apps over traditional credit cards because they seem simpler and more transparent.

Fast Approval Process

BNPL platforms often offer quicker approvals than traditional financing options.

Online Shopping Growth

As ecommerce expanded, retailers embraced BNPL tools to increase conversions and encourage larger purchases.

In many cases, stores actually pay fees to BNPL companies because installment options can increase spending.

Potential Downsides of Zilch

While BNPL services can be useful in emergencies or for budgeting, there are risks too.

Overspending

The biggest issue is how easy it becomes to justify impulse purchases.

A shopper may think:

“It’s only $20 today.”

But if they make that decision repeatedly, multiple payment plans can overlap fast.

Late Fees

Missing payments may trigger penalties or account restrictions.

Budget Confusion

BNPL apps can make it harder to track actual spending because payments are spread out over time.

Debt Stacking

Some consumers juggle several BNPL apps simultaneously, creating dozens of small recurring payments each month.

Financially, it can feel like being pecked to death by very organized ducks.

Is Zilch Safe?

Zilch uses security features common in financial apps, including encrypted transactions and account verification measures. However, like any financial platform, users should:

- Use strong passwords

- Monitor accounts regularly

- Read terms carefully

- Understand repayment schedules before purchasing

The bigger safety concern for many people is not cybersecurity. It’s behavioral spending.

BNPL tools can quietly encourage consumers to spend more than they normally would because the immediate financial pain is reduced.

Final Thoughts

Zilch is part of the growing wave of buy now, pay later platforms reshaping how people shop online and in stores. Its flexible payment options and virtual card system make it more versatile than some competitors.

For disciplined shoppers, BNPL services can help manage cash flow responsibly.

For impulse buyers, though, these apps can become a financial treadmill where every purchase feels smaller until the monthly totals finally arrive all at once.

As with any financial product, the best strategy is understanding exactly how it works before clicking “Pay Later.”