Before I dive into how some Buy Now Pay Later (BNPL) services are costing businesses more than they bargained for, let’s acknowledge the full picture. BNPL has revolutionized how consumers shop and how merchants sell, offering shoppers flexible payments and giving businesses the chance to increase conversions and average order values.

But while there are clear benefits, there’s also a lesser-known side to these services—one that merchants, especially smaller ones, can’t afford to ignore.

BNPL = Buy Now Pay Later

Buy now pay later—now shortened to BNPL—means to buy something now and pay for it over time by making payments. BNPL options, such as layaway, have been around for years, but these services increased in popularity during the pandemic and are still popular among Gen Z and millennial shoppers who like to “split” their purchases into payments.

Over a decade ago, I was one of the first bloggers to research and report about the various buy now pay later services. I wrote how each method worked, how to sign up for the respective service, and then listed the store websites that accepted each particular method which I monetized through affiliate marketing links. I was considered an authority on the subject.

My Affair With Affirm

Affirm was the first BNPL service to catch my attention, and I obviously caught theirs. Starting in 2014, Affirm would email me lists of new stores that they were working with, asking me to add them to my content. After all, I did rank higher in the search engines than they did for key phrases, such as “Affirm stores”.

I had several conversations with Affirm employees over the next few years. I educated them about affiliate marketing and explained how they could make even more money if they were a publisher themselves. I offered to help set everything up for them, thinking it may lead to a consultant gig. Looking back, I was naive. I did not even think about the possibility that what I taught them could potentially put myself out of business.

After Affirm became a publisher (and now adversary), other BNPL services, including Klarna, Quadpay (now known as Zip) and Afterpay, started following suit. I realized that I would need to step up my game or shift focus as I personally didn’t have the resources to compete with those big companies.

Shift of Focus

When the pandemic hit, my traffic, and therefore income, increased dramatically with people trying to make ends meet looking for BNPL services. After receiving an offer that I could not refuse, I was happy to sell my BNPL properties (more on that).

That sale gave me the time and capital to invest in some of my other endeavors, such as my liquidation business. But I missed affiliate marketing, something fierce. So I decided to do some consulting on the merchant side of things. A merchant—or advertiser—is a business that has a product or service to sell.

I recommended to businesses that they should offer buy now pay later services knowing the power they had. I helped merchants set up new affiliate programs and recruit affiliates. I even advocated for merchants to approve the BNPL publishers since they were no competition to me anymore.

The Upside for Merchants

While the fees can be steep, BNPL isn’t all bad news for businesses. In fact, many merchants willingly pay those higher transaction costs because of the upside: BNPL often leads to higher conversion rates, larger average order values, and access to younger consumers who are less likely to use traditional credit cards.

Offering BNPL can also help reduce cart abandonment and drive impulse purchases, especially for more expensive items. For some industries—like fashion, electronics, or furniture—the increase in sales volume can outweigh the added fees. Some merchants even report as much as a 20–30% boost in sales when offering installment options.

So while the costs are real (and rising), many businesses are still choosing to offer BNPL services as a strategic growth tool.

Double Dipping

BNPL companies are similar to credit card processors in that they make money by charging merchants a small percentage of each transaction that uses their service. They may also make money by charging installment fees, interest charges, and/or late payments fees.

According to this article, the typical merchant fee for Affirm is 5.99% + 30¢ per transaction. Compare that to the typical processing fees for Square, which I personally use to process payments, which is 2.6% + 10¢ per transaction.

So, we’ve established that Affirm charges the merchant roughly 6% to process transactions. And according to a 2021 publisher media kit, Affirm was asking for at least 8% commission to even integrate a merchant. For 10% commission, the merchant would get a dedicated merchant page and optimized premium placement across their homepage or categories. And for 12%, Affirm would offer 0% financing, dedicated page and placements on homepage and categories.

Add in the average 2% network fees and another 2% for program manager fees, and merchants are paying out over 20% of their revenue to Affirm which makes it hard to maintain a healthy profit margin.

Stealing Cookies

Most BNPL providers now offer one-time use Visa card numbers to use virtually anywhere. This allows publishers to promote any and all merchants, not just the ones that integrated their services. This also allows these publishers to not only steal the commissions of their competition, but the financing sale as well.

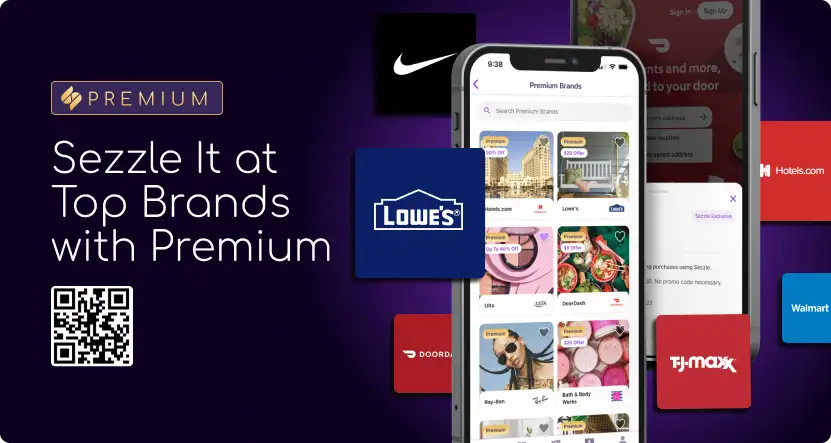

A prime example of this “stealing” is seen right on the Sezzle website. As shown above, they suggest that you can shop now and pay later from “top brands” and include logos for Lowe’s, T.J. Maxx, Walmart, Hotels.com, DoorDash and more. None of those merchants actually use Sezzle as their financing payment processor.

If someone clicks through the Sezzle app to one of those stores (we will use Walmart.com as an example), first a tracking cooking will be set, and Sezzle will be awarded commission for referring the sale. Secondly, Sezzle will give the customer a virtual debit card number to use to purchase. So, Sezzle not only earns the commission but also any fees charged to the customer for financing with Sezzle.

The business ends up paying commission to Sezzle and pays their credit card processor fees to process the virtual Visa card. And the integrated financing provider that the business has chosen to display on their website gets nothing. In this case, Walmart is integrated with Affirm, but Affirm gets nothing.

Final Thoughts

While Affirm has won several awards over the last couple of years being a top publisher in the affiliate marketing industry, their ranking is starting to decline with all of the competitors stealing their thunder. Affirm has bought out a few of their competitors and partnered with others, such as Shopify to power their Shop Pay installments.

Others have joined forces as well trying to get a bigger piece of the pie. Some that come to mind are Zip and Quadpay, Bread Financial and Comenity, Zibby and Katapult, and Klarna and Sofort.

My prediction is that all of the double dipping competition is going to run the small BNPL services out of business (or being bought out by the big guys). I’m presuming that Visa and Mastercard are already brewing their own alternative financing payment options to compete and keep the merchant costs lower. After all, they are already playing the affiliate game.

Now that my no-compete is over, I am pouring my heart into my new personal finance blog because I’m still a money nerd at heart. I’ve applied for a few affiliate programs, but even though I have 25+ years experience in the industry, I’m now considered a “newbie” starting over since I sold off my previous accounts with my websites. So for now, I’ll keep focusing on “creating ridiculously good content” as Ann Handley advises.

- How To File Your 2025 Income Taxes Online For Free In 2026 - January 26, 2026

- The 12-3-30 Workout And Personal Finance - January 9, 2026

- The Power Of Pop-Up Shops - August 24, 2025